Learn More About Stock Trading

It’s All About Today…What About Tomorrow

Canadians are contributing much less to RRSP’s and there is a pattern to far more and more in search of what exactly is available nowadays and allow tomorrow look after by itself. The information stays that it seems we have become much also complacent in planning with only 52% of Canadians contributing to RRSPs in 2011. This can be down from 2010 and has become in decline for your last five years.

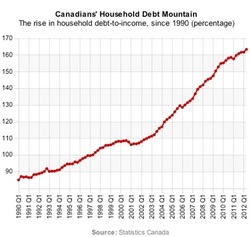

The existing typical family monthly costs exceed month-to-month earnings for 55% of Canadians, with 92% possessing improved their personal debt load more than the previous 5 many years. Canadian household financial debt is documented at 164.62% as being a % of soon after tax income and has been climbing given that 1990. (Source: Statistics Canada- Canadian Home Financial debt Considering that 1990”)

We live for the duration of a time where almost everything is available to us appropriate now, absent will be the days of organizing for a vacation or conserving for any main acquire. This is all available through advertisements offering incentives to “reward yourself now”. The genuine obstacle will be the inflating costs we are sending down the street when it comes to payments and charges that are depleting the ability to put something aside.

Exactly what does all of this really mean? It signifies we could be headed for severe economic concerns if generations aren't preparing for long term increasing rates of interest or for retirement. The truth is Data Canada recently documented 13% of Canadians really feel they're going to never ever have the ability to retire and 30% not till soon after age sixty five. These are alarming figures given we live for the duration of a time of lots.

We also live in the course of a time exactly where countless investing opportunities happen to be created accessible to us. RRSP’s continue to provide tax incentives in which to grow ideas to the long term tax deferred. TFSA’s (Tax Free of charge Cost savings Accounts) give a comprehensive tax-sheltered environment and also the ability to develop this cash without any potential tax implications. The appearance of technology has also raised the bar in terms of self-directed expenditure programs that assist in terms of being aware of when to get and sell inventory opportunities. There exist expenditure programs that leverage the expertise and expertise of seasoned market place traders to get a charge so 1 with little to no information may take advantage and commence buying stocks pursuing a completely guided approach and enjoy the long-term benefits. Some of these programs have routinely documented up to 20% yearly portfolio gains for their consumers.

$5,000 invested inside a TFSA earning 20% each year compounded for 10 many years quantities to $30,958. Gains such as this when utilized to investing $5,000 annually in a TFSA at 20% yearly returns totals $155,752 after ten years. There is certainly no cause why we must give anything up for nowadays to create certain we've got for tomorrow.

This article is actually a shot across the bow and is intended to immediate your interest to what is accessible as well as the time it takes to put in spot your potential plans. Yet another essential statistic is the fact that we're residing longer with average life expectancy for guys at seventy eight.eight and girls at eighty three.three years. So doesn’t it sound right that we strategy to live for a longer time getting the funds to complete so easily?

Other Key Figures (Supply: Canada Statistics)

Canadians’ capability to retire

53% of Canadians usually do not contribute to their RRSP every year 74% of Canadians who make over $100,000 each year annually lead for their RRSP; even so, only 26% of Canadians who make much less than $30,000 annually lead yearly for their RRSP. 13% of Canadians feel that based on their own present scenario they'll in no way have the ability to retire and only 4% of Canadians really feel they're going to be capable of retire ahead of the age of fifty. 30% of Canadians feel they will not have the ability to retire until soon after the age of sixty five.

Canadians are spending greater than they are earning

55% of Canadians have monthly expenses that exceed their monthly income at least when a 12 months. 92% really feel that Canadians have a lot more debt than they did five many years ago, nonetheless, only 7% perceive that it tends to make more perception to hold a larger volume of debt now against 5 many years ago.

17% of Canadians will ought to make significant alterations to paying routines and will have to think about an motion strategy to help steer clear of bankruptcy if their revenue had been to drop by 10%. For 14% of Canadians, their monthly expenditures exceed their month-to-month income greater than 6 months of the 12 months 6% of Canadians have costs that exceed their monthly income 12 months on the yr.

Some Canadians aren't aware of the effect of interest rates

26% of Canadians don't think about the results of a rising rate of interest when borrowing cash

28% of Canadians usually do not know the interest rate on their own charge cards.

Several Canadians require credit schooling

80% of Canadians don't know their credit score

63% of Canadians do not know how their credit score is established

40% of Canadians usually do not pay their bank card off in full every month

86% of Canadians believe that a lot more Canadians are in credit score distress now than they had been 5 many years in the past.

53% of Canadians think that credit score is also easy to receive in Canada

43% of Canadians have more than three bank cards

37% of Canadians only pay the minimum required amount on their own credit card each month opposed to paying out it off in full

14% of Canadians are shocked by the amount owed on their bank card after they get the monthly bill

30% of Canadians have a total stability on their own bank card each month which is greater than $1000 (on average)

Only 37% of Canadians who make significantly less than $30,000 each year spend their bank card off in complete each month; while 73% of Canadians who make $100,000 each year pay it off in complete every month

Canadians’ perception in the housing marketplace

58% of Canadians really feel that in the next 24 months, the housing market will continue to grow and prices will increase

42% of Canadians think the housing industry will remain precisely the same or decline within the next 24 months

4% of Canadians think that inside the next 24 months, the housing market place will decline by greater than 10%

The existing typical family monthly costs exceed month-to-month earnings for 55% of Canadians, with 92% possessing improved their personal debt load more than the previous 5 many years. Canadian household financial debt is documented at 164.62% as being a % of soon after tax income and has been climbing given that 1990. (Source: Statistics Canada- Canadian Home Financial debt Considering that 1990”)

We live for the duration of a time where almost everything is available to us appropriate now, absent will be the days of organizing for a vacation or conserving for any main acquire. This is all available through advertisements offering incentives to “reward yourself now”. The genuine obstacle will be the inflating costs we are sending down the street when it comes to payments and charges that are depleting the ability to put something aside.

Exactly what does all of this really mean? It signifies we could be headed for severe economic concerns if generations aren't preparing for long term increasing rates of interest or for retirement. The truth is Data Canada recently documented 13% of Canadians really feel they're going to never ever have the ability to retire and 30% not till soon after age sixty five. These are alarming figures given we live for the duration of a time of lots.

We also live in the course of a time exactly where countless investing opportunities happen to be created accessible to us. RRSP’s continue to provide tax incentives in which to grow ideas to the long term tax deferred. TFSA’s (Tax Free of charge Cost savings Accounts) give a comprehensive tax-sheltered environment and also the ability to develop this cash without any potential tax implications. The appearance of technology has also raised the bar in terms of self-directed expenditure programs that assist in terms of being aware of when to get and sell inventory opportunities. There exist expenditure programs that leverage the expertise and expertise of seasoned market place traders to get a charge so 1 with little to no information may take advantage and commence buying stocks pursuing a completely guided approach and enjoy the long-term benefits. Some of these programs have routinely documented up to 20% yearly portfolio gains for their consumers.

$5,000 invested inside a TFSA earning 20% each year compounded for 10 many years quantities to $30,958. Gains such as this when utilized to investing $5,000 annually in a TFSA at 20% yearly returns totals $155,752 after ten years. There is certainly no cause why we must give anything up for nowadays to create certain we've got for tomorrow.

This article is actually a shot across the bow and is intended to immediate your interest to what is accessible as well as the time it takes to put in spot your potential plans. Yet another essential statistic is the fact that we're residing longer with average life expectancy for guys at seventy eight.eight and girls at eighty three.three years. So doesn’t it sound right that we strategy to live for a longer time getting the funds to complete so easily?

Other Key Figures (Supply: Canada Statistics)

Canadians’ capability to retire

53% of Canadians usually do not contribute to their RRSP every year 74% of Canadians who make over $100,000 each year annually lead for their RRSP; even so, only 26% of Canadians who make much less than $30,000 annually lead yearly for their RRSP. 13% of Canadians feel that based on their own present scenario they'll in no way have the ability to retire and only 4% of Canadians really feel they're going to be capable of retire ahead of the age of fifty. 30% of Canadians feel they will not have the ability to retire until soon after the age of sixty five.

Canadians are spending greater than they are earning

55% of Canadians have monthly expenses that exceed their monthly income at least when a 12 months. 92% really feel that Canadians have a lot more debt than they did five many years ago, nonetheless, only 7% perceive that it tends to make more perception to hold a larger volume of debt now against 5 many years ago.

17% of Canadians will ought to make significant alterations to paying routines and will have to think about an motion strategy to help steer clear of bankruptcy if their revenue had been to drop by 10%. For 14% of Canadians, their monthly expenditures exceed their month-to-month income greater than 6 months of the 12 months 6% of Canadians have costs that exceed their monthly income 12 months on the yr.

Some Canadians aren't aware of the effect of interest rates

26% of Canadians don't think about the results of a rising rate of interest when borrowing cash

28% of Canadians usually do not know the interest rate on their own charge cards.

Several Canadians require credit schooling

80% of Canadians don't know their credit score

63% of Canadians do not know how their credit score is established

40% of Canadians usually do not pay their bank card off in full every month

86% of Canadians believe that a lot more Canadians are in credit score distress now than they had been 5 many years in the past.

53% of Canadians think that credit score is also easy to receive in Canada

43% of Canadians have more than three bank cards

37% of Canadians only pay the minimum required amount on their own credit card each month opposed to paying out it off in full

14% of Canadians are shocked by the amount owed on their bank card after they get the monthly bill

30% of Canadians have a total stability on their own bank card each month which is greater than $1000 (on average)

Only 37% of Canadians who make significantly less than $30,000 each year spend their bank card off in complete each month; while 73% of Canadians who make $100,000 each year pay it off in complete every month

Canadians’ perception in the housing marketplace

58% of Canadians really feel that in the next 24 months, the housing market will continue to grow and prices will increase

42% of Canadians think the housing industry will remain precisely the same or decline within the next 24 months

4% of Canadians think that inside the next 24 months, the housing market place will decline by greater than 10%